The Bank of Canada is making a rate announcement Wednesday, July 24th.

Here’s what you need to know:

- A fundamental review.

- Inflation outlook.

- Risk review.

Bank of Canada Fundamentals:

- The Bank of Canada makes eight interest rate announcements per calendar year. At these announcements the Bank will either 1) raise rates, 2) lower rates, or 3) do nothing.

After the rate announcement on July 24, the next interest rate announcement is September 4th, and then October 23rd. - Moving Canada’s key lending rate is primarily an effort to achieve the Bank of Canada mandate of 2% inflation. An acceptable range of inflation is 1-3% (also referred to as the “target range”).

- In general, lowering interest rates helps stimulate short term borrowing (credit growth) which boots the economy, leading to higher inflation. In general, raising interest rates restricts short term credit growth which cools the economy.

- When the Bank of Canada raises or lowers Canada’s central interest rate that raises or lowers the commercial bank (RBC, CIBC etc) Prime interest rate.

The Prime rate is linked to personal lines of credit, student loans, business loans, and variable rate MORTGAGES. - There is a distinction between fixed interest rates and variable interest rates. Fixed interest rates move based on Canada bond yields. Variable interest rates move based on changes to the Prime rate. Changes to the Prime rate happen when the Bank of Canada changes the key lending rate.

Over a long enough time horizon, fixed and variable rates do move in the same general direction—although their mechanism for movement is different. - Today, before the July 24th rate announcement, the Key Lending rate (set by the Bank of Canada) is 4.75%. The Prime lending rate is 6.95%.

- The market consensus is for the Bank of Canada to lower interest rates by 0.25% on July 24th.

Inflation Outlook:

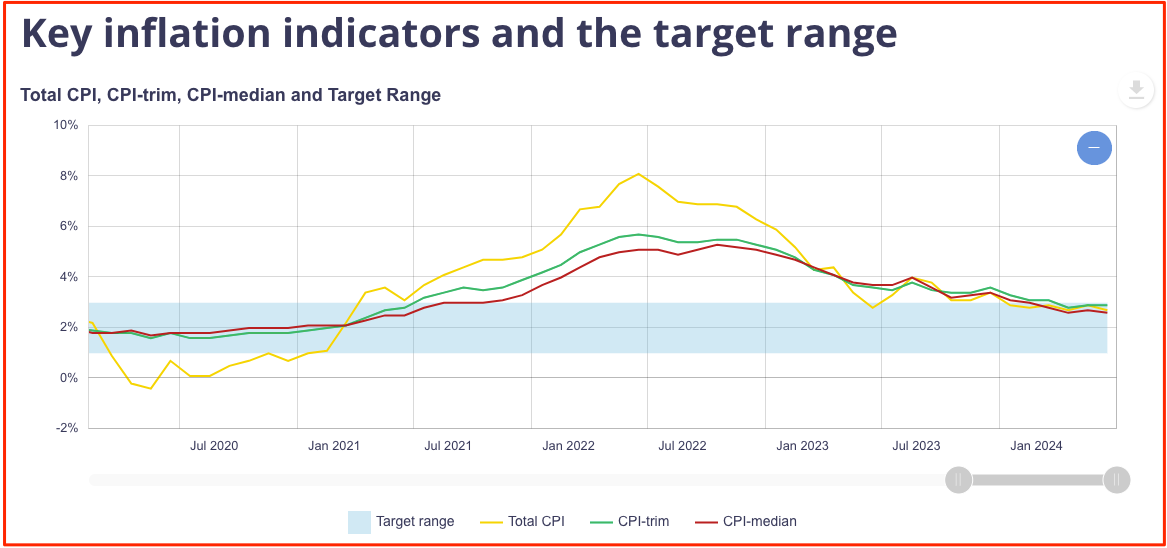

Below is a chart showing the latest Consumer Price Index (CPI) data. The Consumer Price Index is the name of inflation in Canada.

Remember, inflation is the change of prices compared to one year ago. A lower inflation rate still means prices are rising, just at a slower rate.

We can see a slow trend of headline CPI and several other core measures of CPI all trending to the “target range” of 1-3%.

Core measures of inflation were created about 10 years ago for the Bank of Canada to monitor inflation with and without various items in the inflation weighting basket.

The world is also keenly watching how inflation, and interest rates are evolving in the United States.

U.S. inflation data came out last week, lower than market expectations. U.S. consumer price index is 3.0%. A Federal Reserve rate cut in September is a growing possibility. This helps the Bank of Canada possibly cut rates, without straying too far from the U.S. Fed.

Risks To The Inflation Outlook:

Risks to the inflation outlook mean areas of interest the Bank of Canada have highlighted that can possibly create a meaningful change toward the 2% inflation target.

- Mortgage renewals. Over 50% of Mortgage holders have yet to renew into higher rate Mortgages. This will increase their shelter component, leaving less money for discretionary spending.

- Strong wage growth. Wage growth is still around 4%, which is higher than the inflation target.

- Rate cuts and housing. Rate cuts could lead to an overheating of the housing market, spurring inflation.

- Rapid unwinding of immigration. A record number of new people being added to Canada is boosting inflation. A shock in the other direction is a risk.

- Everything. Geopolitical tension, labour disruptions, climate events, price of oil, supply chains, inflation.

Conclusion:

The market consensus is increasing the possibility of the Bank of Canada cutting interest rates by 0.25% in July based on a lower Consumer Price Index print in both the U.S. and Canada.

For every $100,000 of Mortgage, a 0.25% rate cut equals about $15/month payment decrease. Therefore, a $400,000 Mortgage holder would see their payment drop by about $60/mo.

If you are currently in a fixed rate Mortgage, your payment does not change.

I’m continuing to see fixed rate Mortgages grind lower. This is better news for everyone planning to renew their Mortgage in about 12-18 months.

Two common themes for Mortgage selection today are a 3-year fixed rate Mortgage, and a 5-year fixed rate Mortgage.

The thinking with a 3-year term is your renewal date would be two years sooner than the longer duration 5-year term. The idea is you would be renewing into a lower interest rate environment.

The thinking with a 5-year term is the rate is low and worthy to be locked in. We all agree today’s 5-year fixed rate is higher than pandemic, and great financial crisis rates (GFC)—but still low.

I think it’s fair to say great financial crisis and pandemic era rates were artificially manipulated lower. Today’s rates are much less manipulated. With this context, today’s 5-year rates are not that bad.

Some folks also want a 5-year rate so they’re not having to worry about their Mortgage for a longer time.

Eventually, the consideration of a variable rate will come back into conversation.

Only with the benefit of hindsight will we know if a 3-year term or 5-year term Mortgage was best.

I hope this rate preview is helpful! If you have any questions, reach out!

Talk soon,

Chad Moore

P.S.

If you’re thinking of moving, and are curious how to decide about sale-purchase order—I’ve written you some ideas on how to navigate that decision. I’ve titled the pdf “The Ultimate Home Transition Blueprint—Checklist” (link).