Like a good soap opera, the Canadian (and Global) economy is providing us with drama, cliff hangers, key characters and many different story lines. Below is a simplified version of what I think you need to understand:

The lower outlook for Canadian growth has increased the downside risks to inflation. While vulnerabilities associated with household imbalances remain elevated and could edge higher, Canada’s economy is undergoing a significant and complex adjustment. Additional monetary stimulus is required at this time to help return the economy to full capacity and inflation sustainably to target.

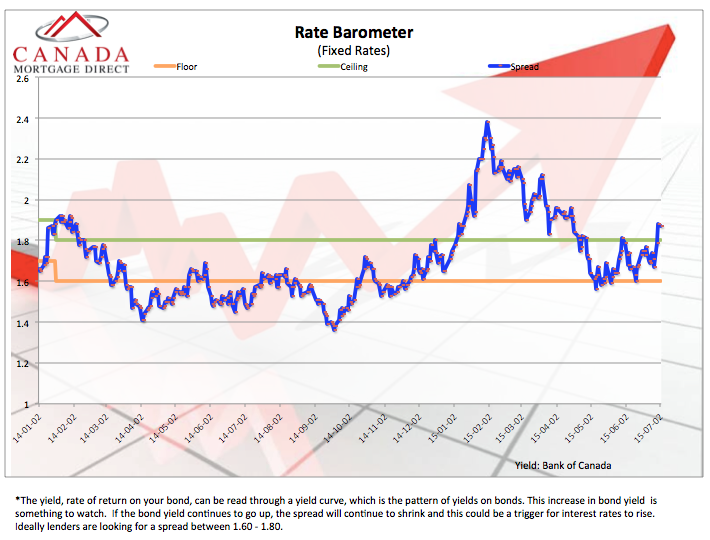

Fixed interest rates are derived form Canada’s bond market. They are not directly tied to the BoC’s key lending rate, but they do trend with this rate over time.

Banks take deposit money, in the form of Bonds, and fractionally lend that money out in the form of Mortgages. Banks lend this money out at higher yields to profit from the risk of lending. This yield is also referred to as “the spread”.

In the image below, you’ll notice the blue line moving up and down over time. This is “the spread” Banks are making from fixed interest rate Mortgages. Note the increasing spread recently. This allows Banks to lower their fixed interest rates and still maintain a comfortable level of profitability.

Well, the low interest rate party continues.

Low interest rates allow you to qualify to borrow more money. If you can borrow more money, you may purchase a more expensive home. Really, I think the BoC hates reducing rates because they are worried about over inflating (continuing to?) the housing market.

Here is the thing …our fragile economy may continue FOR YEARS. I mean, look at the head wind we’re facing (low rates, increasing home costs, down oil, lower demand for exports, global uncertainty, AB political change – and more).

Despite all of this going on, people still want to purchase a home. The bottom line is, if you have stable employment (or the thought of stable employment) and wish to purchase a home, I am willing to help you understand your options.

Yes, a home is a large investment and the price may fluctuate over time. So do other investments. I think the key is to simply understand your options, speak to trusted advisors and do the best you can.

So, if you have the thought home ownership is a part of your overall financial portfolio …

If you are 6-12 months away from purchasing a home, the housing and interest rate market should be of keen interest to you. You may already be thinking about looking at homes for sale online.

If you’re like many home buyers, you’re probably wondering how much you can afford to purchase? Or you would like to understand what the true cost of home ownership is. You can look at homes for sale online for hours, but without really understanding your purchasing power, I think that’s a waste of your time.

I want to help you narrow down your home search, save you time and money. I want to help you specifically understand how much you can afford to purchase.

I make time to lead all of my clients through a step-by-step Mortgage approval plan that is customized for each of my clients. I strive to minimize your time investment and maximize the results you want, which is clarity and confidence in your Real Estate understanding.

I do this to earn your business, testimonials and future referrals.

100% no obligation. 100% risk free.

Your fist step is to enter your email address into the form below. Step two is understanding your home affordability and pin pointing your home search.

Of course it takes a special person to strategically and methodically plan long before purchasing a home. Even though I am selective in who I invest my time with, I know only a small portion of you reading this message now will take me up on this free offer. Banks count on the fact many people truly do not understand their Mortgage options. Can you afford to pay more for your Mortgage than you should?

Thank you for reading :-)

Talk soon,

Chad Moore

P.S

Yes, our economy is facing large headwinds. I am not glossing over the fact our economy is seemingly fragile right now. I also take the position there is an opportunity in every scenario.

When you understand your home purchasing power you are able to make clear and confident decisions about your living accommodations. You take control. You take ownership. You make decision.

I want to help you understand everything. Be sure to enter your email address by clicking the above image to get started.

P.P.S

Please click the “Like” button at the top of this post to let me know you enjoy this content. Thank you in advance (-:

Here are some Calgary Real Estate numbers, across all property types, out of the gate for…

Hey Guys! Tariffs are here. Now what? Tiff Macklem, governor of the Bank of Canada, gave…

Hey Guys! The Bank of Canada publishes "meeting deliberation notes" relating to the discussion of raising,…

When the governor of the Bank of Canada speaks, we listen! Tiff Macklem, governor at…

Let's look back at January 2025 Calgary Real Estate Board (CREB) data to make sense…

Hey Guys! Here's an example of how the Bank of Canada is in a balance…

{kind=link}