Hey Guys!

Let’s look back on 2024, compare it to previous years’ and make reasonable near term predictions for the market looking forward.

I’ve upgraded the apartment data to look back 10 years. We’re now looking back at 10 years of detached and apartment data.

Looking back on 10 years of data will showcase two very different Real Estate seasons in Calgary. This is also a reminder that Real Estate cycles.

For both detached and apartment housing, let’s look at the following:

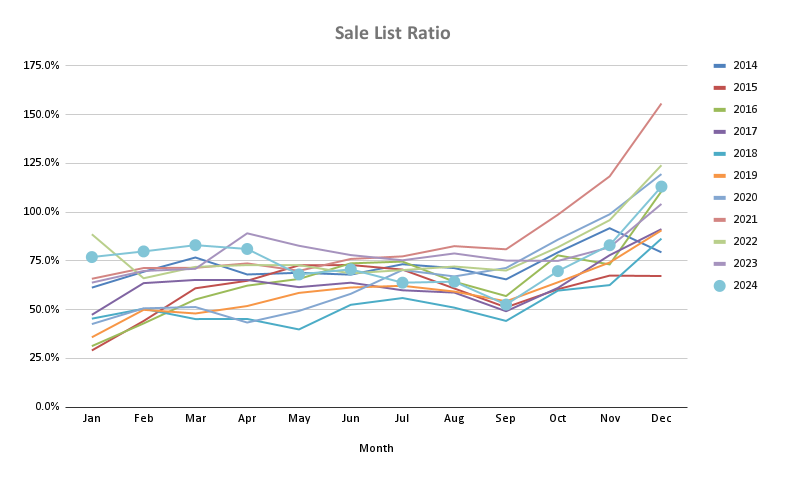

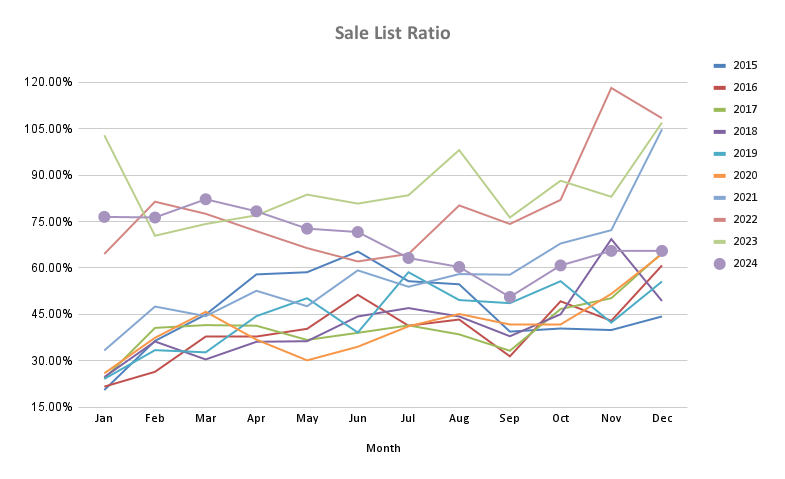

The sales to new listings ratio is a simple indicator of near term housing supply growing or shrinking.

The blue December 2024 dot is above 100%. This means there were more sales than new listings. This means there are now less homes for sale than before.

The sale to new listing ratio nearly always increases in December. However, cresting over the 100% line has only happened since 2020. And this is a leading indicator that the Spring market will be undersupplied, again.

If demand for Calgary detached homes is about the same, and supply is lower, then that is a recipe for home buyer competition and prices to increase, again.

If you know of first time home buyers that are thinking of purchasing this Spring, they might want to anticipate a very competitive purchase market. Or they might want to delay their purchase until later in the year, or pull their purchase forward.

For those selling and purchasing in the same Spring market, you’re likely to sell high, and then purchase high.

Check out the three graphs below to compare previous years of how the data evolved.

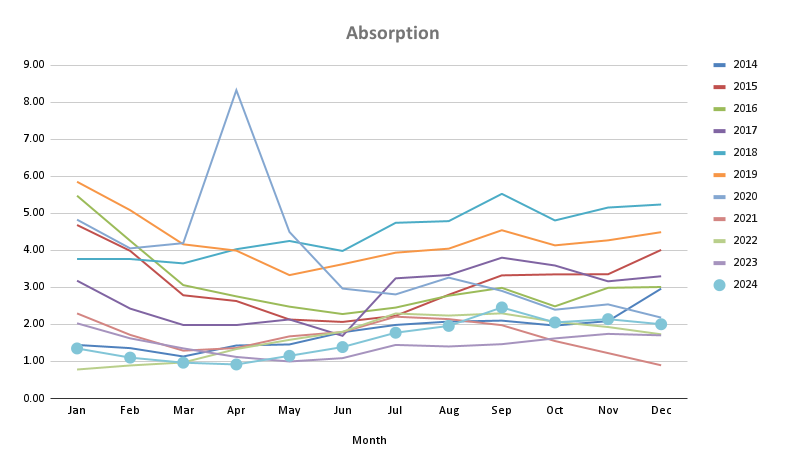

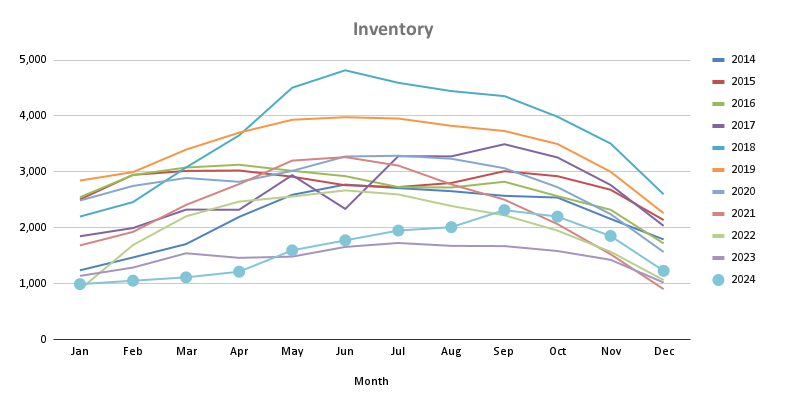

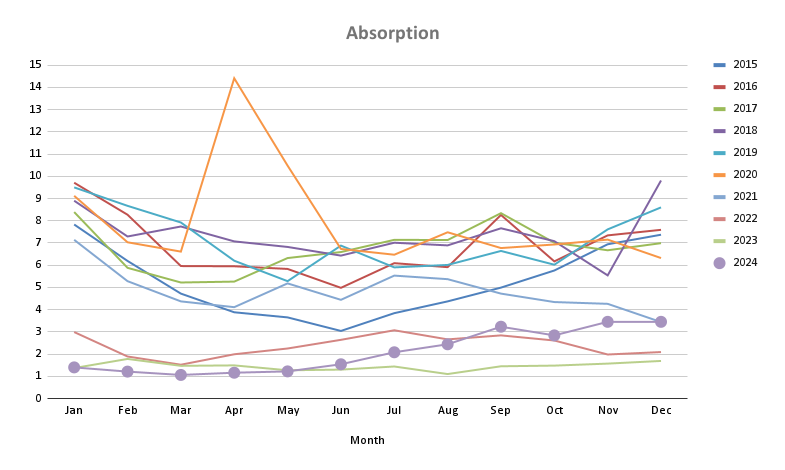

The absorption rate tells us how many months of inventory we have. If Calgary were to sustain the current inventory level, and the current sales numbers—how many months of inventory would we have. This ratio answers this question.

With the sales to new listings ratio cresting over 100% let’s not be surprised if Calgary detached absorption rate dips below 2 months of inventory.

I consider an absorption rate below 2 months as a undersupply crisis. And in a crisis people’s behavior changes. Over the past 3-4 Spring markets the competition for housing has produced risky behavior of buyers (I.E., no or little purchase conditions (not recommended)).

Again, buyers are wise to plan for a highly competitive market starting in about March and lasting to about the end of June. I have notice purchase agreements starting to have conditions again around that time.

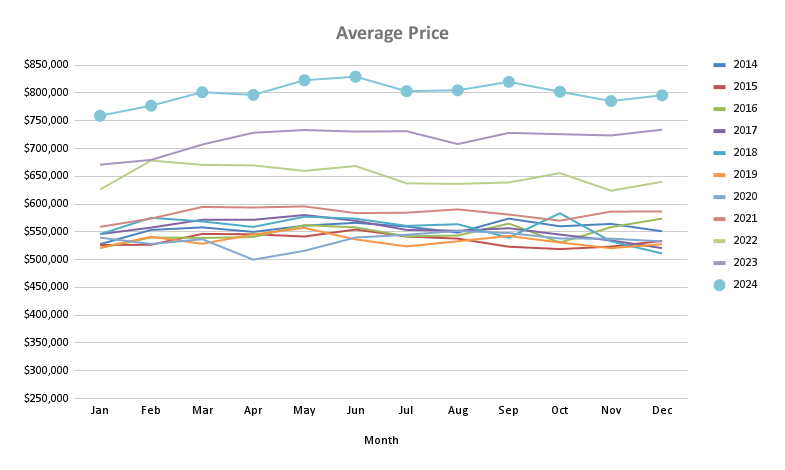

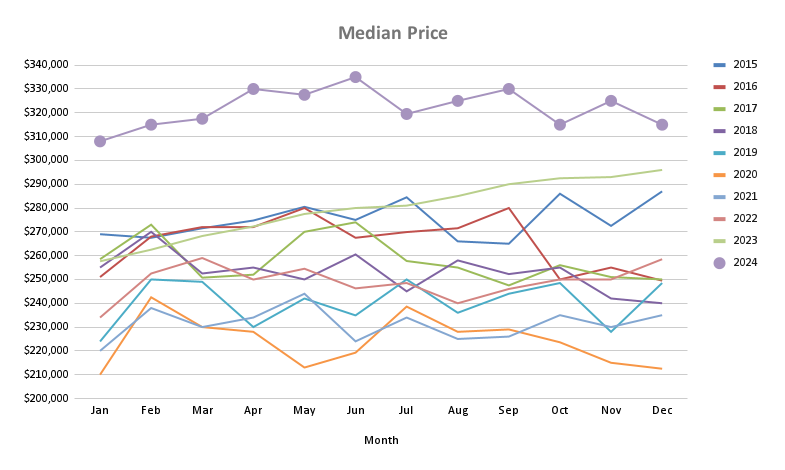

The average price of a detached home is about flat since April. The back half of 2024 saw prices soften, slightly.

The back half of also had 1.75% of interest rate cuts from the Bank of Canada. The stimulus of rate cuts takes 12-18 months to appear in the economy.

You can see the stark difference between the detached sales to new list ratio, and the apartment sales to new list ratio. The apartment ratio is much lower, indicating the accumulation of inventory.

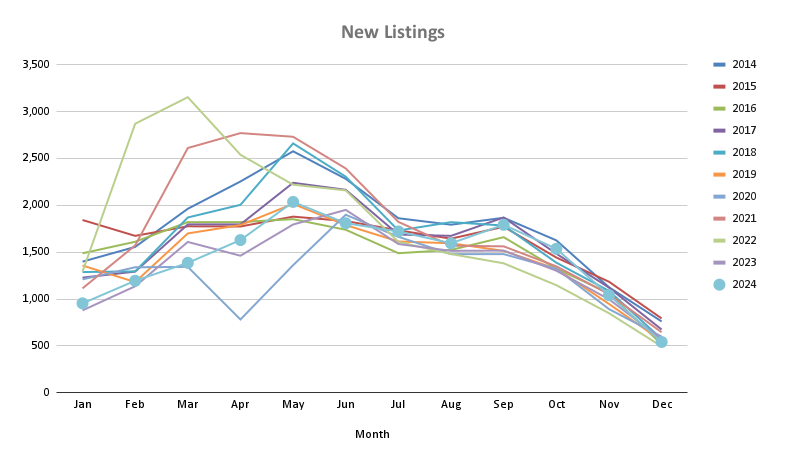

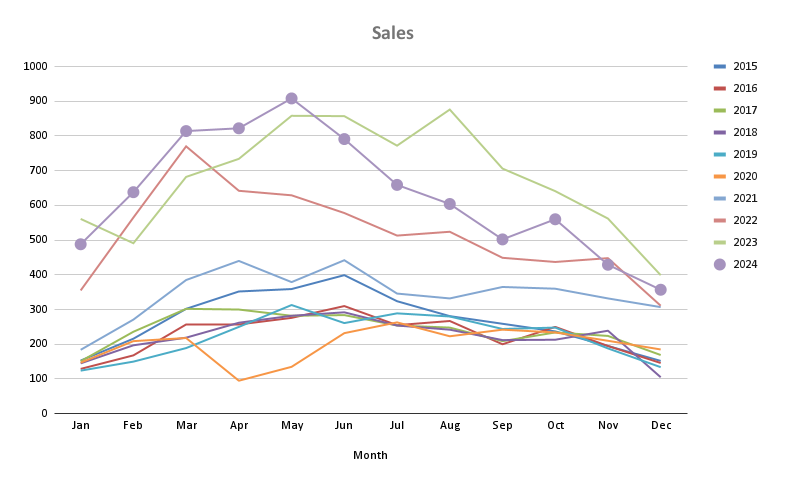

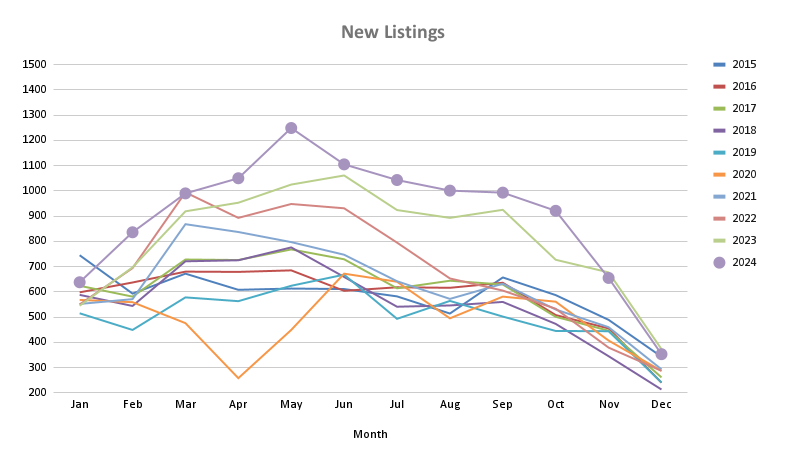

New listings seasonally drop off, as they have in previous years. But new listings are higher relative to previous years.

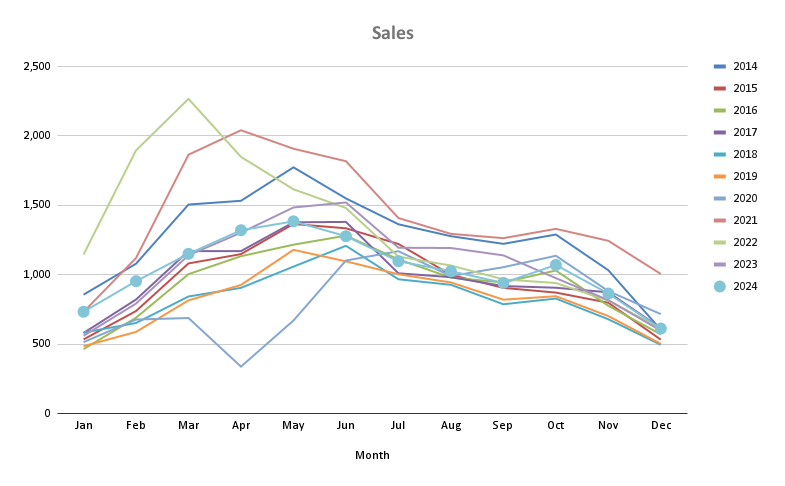

Scrolling down to the sales chart …we can see sales are strong, but with a higher new listing month, there is still inventory growing.

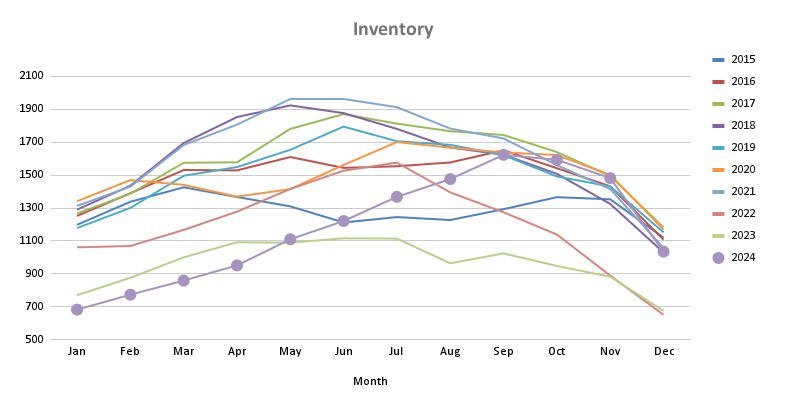

Look at the absorption rate, and the total inventory chart below. Inventory started very low, but grew and grew throughout the year.

We can also see the absorption rate grow over this same period. There is a lot more balance in the apartment market, compared with the detached market.

2024 median pricing was a giant leap higher for Calgary apartments. Median price is up for the year, but flat since about February ’24.

The combination of higher absorption rate and lower sales to new listings ratio, is setting up median apartment prices to soften (come down lower). It’s possible there is downward pressure of apartment prices.

The Bank of Canada interest rate announcement schedule is:

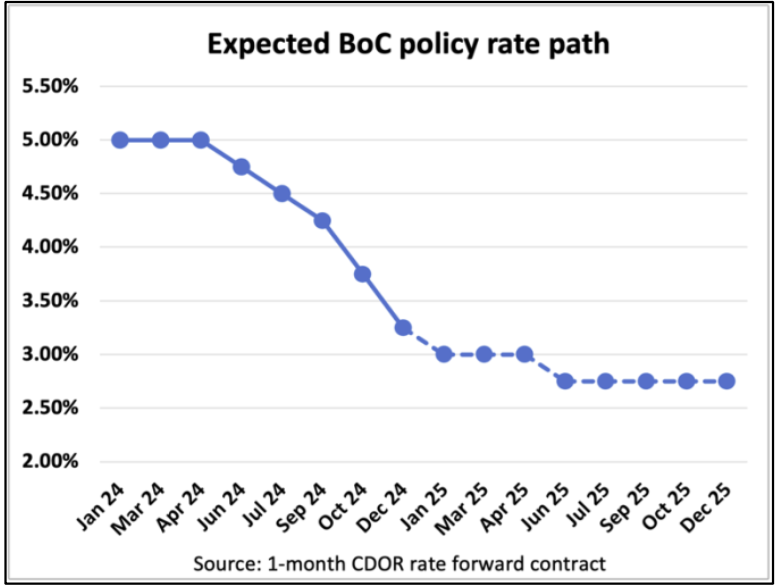

Below is an image of the cuts the Bank of Canada has made in 2024, and a prediction of rate cuts moving forward for the next 12 months.

Let’s watch how these rate cut expectations evolve throughout the year.

It’s looking like Calgary’s detached housing market is still undersupplied leading into the busiest time of year. I say this because the sales to new listing ratio crested 100% in December, with an already low months of inventory (2 months). This could lead to competitive bids, emotional buying behavior, and reasonable price support this Spring.

Calgary’s apartment market is setting up to be much different. The sales to new listings data is much lower, with a rising absorption rate. Apartments are at peak median pricing, so it’s possible we see those numbers edge lower.

The Bank of Canada outlook is lower interest rates. It’s looking like we are entering a cut-pause era of monetary policy (this is seemingly more normal).

Let’s be reminded, fixed interest rates move up and down based on the the bond yields. Fixed interest rates do not directly move up and down based on Bank of Canada rate cuts, or rate increases. Variable Mortgage rates move in lock step with changes to the Prime rate—and the Prime rate is linked to the Bank of Canada.

I hope this is helpful!!

Talk soon,

Chad Moore

Here are some Calgary Real Estate numbers, across all property types, out of the gate for…

Hey Guys! Tariffs are here. Now what? Tiff Macklem, governor of the Bank of Canada, gave…

Hey Guys! The Bank of Canada publishes "meeting deliberation notes" relating to the discussion of raising,…

When the governor of the Bank of Canada speaks, we listen! Tiff Macklem, governor at…

Let's look back at January 2025 Calgary Real Estate Board (CREB) data to make sense…

Hey Guys! Here's an example of how the Bank of Canada is in a balance…

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}