Hey Guys!

Amidst a federal political meltdown, let’s stay updated on Canadian Mortgage interest rates ((tl;dr ;-) if you scroll, read the bold)) …

Here’s what I have for you:

Question for you …if the Bank of Canada cuts interest rates, does that mean fixed interest rates also move lower?

Here’s what the last 5 months of Bank of Canada rate cuts have looked like:

That’s 1.75% rate cuts since the summer—WOW! The next Bank of Canada rate announcement is January 29th, 2025.

Remember this now …The commercial Prime rate has come down by the same rate cut factor the Bank of Canada has made (1:1). The Prime rate was 7.20%, and today the Prime rate is 5.45%.

The Prime rate is what variable rate Mortgages are priced from. To be clear, the Bank of Canada raises or lowers the central interest rate (now 3.25%) and the commercial Prime rate moves in kind (Prime rate now 5.45%).

(Side note: there has been two times when the Bank of Canada cut rates by 0.25% and the commercial Prime rate only dropped by 0.15%. Banks. Owe. Us.)

What does this mean for variable rate Mortgage payments …??

On a $400,000 Mortgage, with a 25 year amortization, a Mortgage payment has come down ~$325/mo since the summer.

Where might rates go from here??

The forecast is more rate cuts.

Why?

The current interest rate level is still deemed to be restrictive (too high for the current state of our economy).

There is mounting economic data outlining that high rates have finally bitten the economy, and are no longer warranted.

So how many more rate cuts is “the market” predicting?? I’m reading the Bank of Canada central interest rate could land in the 2.00% to 3.00% range.

This would mean between 0.25% to 1.25% more rate cuts are ahead of us. The Bank of Canada is looking for a theoretical “neutral interest rate” that is neither stimulative, or restrictive.

NOTE: there is an incredible amount of economic uncertainty on the horizon (as there always is). New tariffs imposed on Canada is one new concern. And another concern is near term negative population growth.

Fixed and variable rates do not directly move up and down together!

As mentioned above, when the Bank of Canada raise or lower the central interest rate, that effects the Prime interest rate. The Prime rate is what variable rate Mortgages are priced from.

Fixed interest rates are priced from bond yields. For example, people make deposits of money for the which the bank pays them a yield—say 2-3%.

The bank turns around and lends that money out at 4-5%. Deposit taking banks pay a yield on the money to the depositor, but lend that money out at higher interest rates in the form of a Mortgage. This is one way banks make a profit.

So, when deposit yields go up, banks raise fixed interest rates to retain their profit margin. When yields go lower, banks complete for new business by lowering their fixed rates.

This is an incredible simplification of the system, but the fundamental to remember is fixed rates move based on bond yield moves.

And here is where A LOT of folks are confused …people are seeing the Bank of Canada cut rates—and think fixed rates are down too.

The “rate cut” narrative has completely seeped into the main stream—but people think that automatically means fixed rates are lower. They are not.

Read below as to why fixed rates are UP.

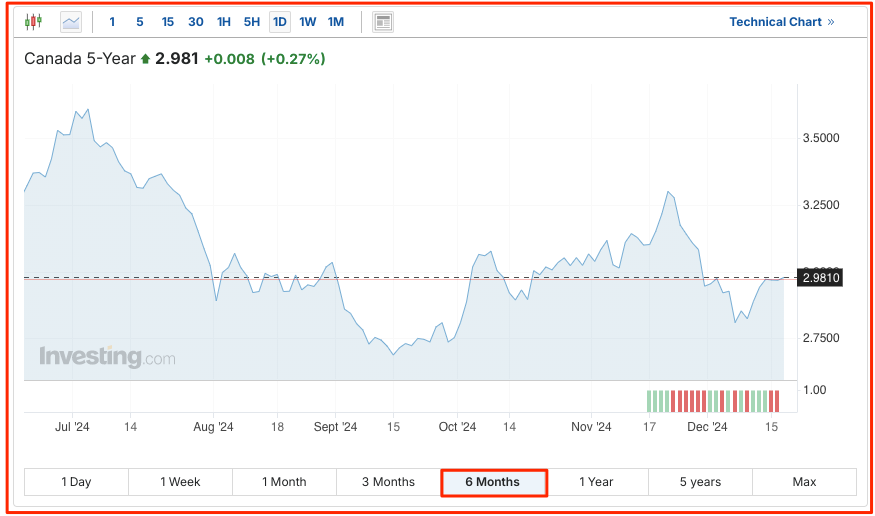

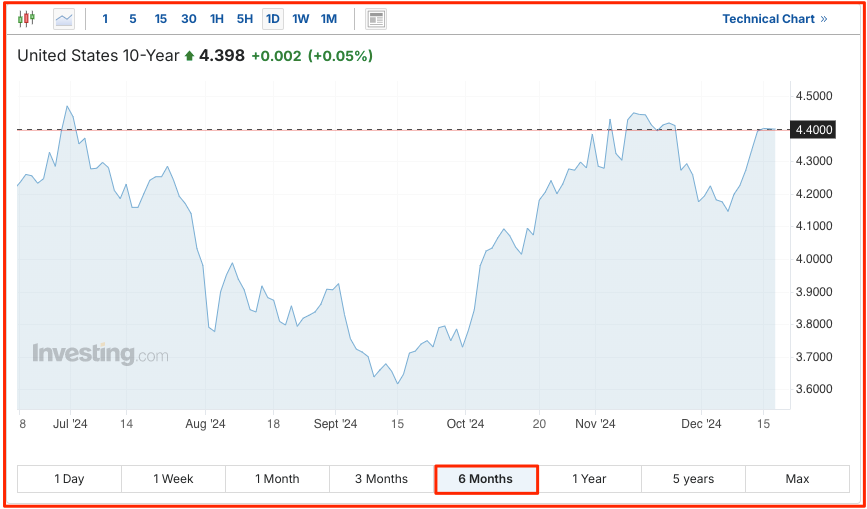

U.S. Treasury Yield + Canadian Bond Yield:

Below is a 6-month look back of two images, a) Canada 5-year bond yield curve, and b) U.S. Treasury yield curve. Are you seeing the similarities?

Canada’s bond market is historically pulled around by the U.S. Treasury market.

You can see from September to current, in the midst of steep Bank of Canada rate cuts, fixed Mortgage interest rates are seeing upward pressure.

To be fair, fixed and variable interest rates historically move in the same direction—we would need to zoom out on a chart with the perspective of decades. Zooming in on a 6-month period can showcase divergent fixed and variable interest rate scenarios.

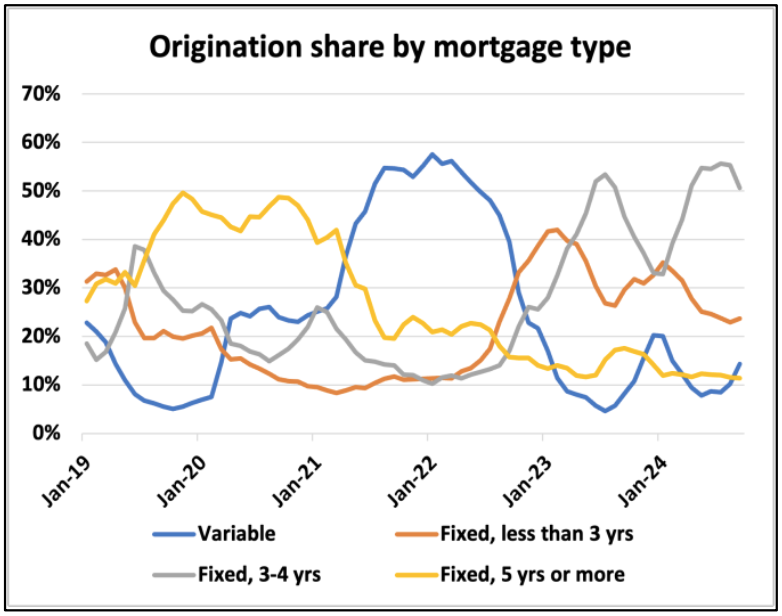

Mortgage Product Of Choice:

Below is a chart of what Mortgage product other Canadians are selecting.

The decision of Mortgage product, for each individual or couple, is personal. Everyone is at various stages of life, has their own risk tolerance level, personal financial situation, and outlook on the economy.

I showcase this information because I am often asked about what Mortgage product/type other’s are choosing.

Some folks are dead-set on a variable rate Mortgage. Other’s cannot be bothered to think about the outlook of interest rates, and therefore want a fixed rate.

Other’s choose a hybrid approach. The hybrid approach is to start with a variable, then plan on converting their Mortgage to a fixed rate.

For those renewing their Mortgage in the next 18 months, plan to renew at a higher Mortgage rate (shocking take ;-)).

If your rate is set to double, that does not mean your payment will double. Here are some examples …

2020 Mortgage:

$400,000 balance

25 year amortization

2.10% fixed rate

$1,713/month

2025 Mortgage:

$335,785 balance

20 year amortization

4.49% fixed rate

$2,241/month

The monthly payment in this example increased by 31% or by $528/mo.

One idea to lower a Mortgage payment is to refinance. If applicable, the benefit of a refinance is to consolidate other high interest debts and increase the amortization of your Mortgage.

By consolidating debt, and spreading the Mortgage out over a longer period, the overall monthly payment can be lower.

Refinance Mortgage:

$350,000 balance (higher balance to consolidate debt)

30 year amortization

4.84% fixed rate

$1,756/month

Note: spreading a Mortgage out over a longer time period dramatically increases the total interest paid by the borrower. A refinance needs to be carefully thought through.

The Bank of Canada has slashed interest rates by 1.75% since the Summer. Fixed interest rates have been propped up by the U.S. Treasury Yield.

Canadian Mortgage holders are still shying away from variable rates, for the moment. Many people are seeing the wisdom of a 3-year fixed rate. A 3-year fixed rate might prove to be a good combination of stability, and flexibility.

About 40% of Mortgages will be renewing in the next 18 months. For many folks, this means higher interest rates and payments. One idea is to use home equity to consolidate high interest debt, and spread the Mortgage out over a longer time horizon (this is not a blanket recommendation, FYI).

In amongst all the political news hitting the airwaves, new Mortgage lending programs are being released. I’ll have more on these policies, soon.

Cheers,

Chad Moore

Here are some Calgary Real Estate numbers, across all property types, out of the gate for…

Hey Guys! Tariffs are here. Now what? Tiff Macklem, governor of the Bank of Canada, gave…

Hey Guys! The Bank of Canada publishes "meeting deliberation notes" relating to the discussion of raising,…

When the governor of the Bank of Canada speaks, we listen! Tiff Macklem, governor at…

Let's look back at January 2025 Calgary Real Estate Board (CREB) data to make sense…

Hey Guys! Here's an example of how the Bank of Canada is in a balance…

{kind=link}

{kind=link}

{kind=link}

{kind=link}