There is a NEW method to determine the minimum down payment when purchasing a home, scheduled to take effect February 15th. This will affect your home sale and purchase. But first …

I would like to thank the Canadian Department of Finance for using a scalpel instead of a sledgehammer to temper the Canadian housing market.

Clearly, the super heated (and consistent) housing markets of Toronto and Vancouver is at the top of our Canadian Governments list to cool. This rule change does affect Alberta’s housing market, and we now live with this coming change.

Let’s review the changes of down payment requirements, study what they actually mean in dollar figures and hypothesize what might happen as a result.

First a brief and non-technical explanation of down payment rules in Canada. A down payment less than 20%, of the purchase price of the home, requires Mortgage insurance.

Mortgage insurance protects the Mortgage lender from incurring any loss because of default (non-payment) on the loan. A one time insurance premium is added into the Mortgage, paid by the borrower. The lower percentage down payment a buyer makes, the higher the Mortgage insurance premium is, up until 20% when there is no premium required. Mortgage insurance is only available on home purchase prices less than $1M dollars.

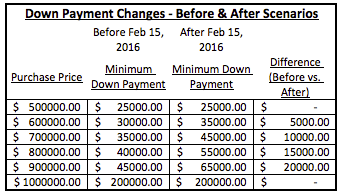

Ok, here is a list of the NEW Minimum Down Payment requirements in Canada.

For new buyers in Canada, what does this actually mean? Let’s look at before and after scenarios of purchasing a home from $500K to $1M with and without the new down payment regulations.

The reality is the down payment requirements to purchase a home over $500K are more money.

Quite frankly, I applaud the Department of Finance for implementing this rule. In other major markets, the segment of home values from $500-$999K are seeing large price advances. I think taking measures to slow this segment is wise.

However, WE do not live in Toronto or Vancouver. I am told the price range of homes $750K+ in Calgary is already under the most downward pricing pressure. I think this Mortgage rule change certainly adds fuel to the already burning fire.

Home buyers without an additional five to ten thousand dollars for down payment of a five hundred or six hundred thousand dollar home will either have to save more money, delaying their home purchase by months or years.

Alternatively, these potential buyers might have to reduce their price range search to $500K or less. This might create more demand for property in the lower price ranges because people do not want to wait to save more money OR do not have access to gift money for down payment.

Many of the first time homebuyers I help do inherit money from their immediate family for their down payment. Could these new Mortgage rule changes result in the Boomer generation tapping into more of their nest eggs to help their children enter the housing market? I think so.

In conclusion, navigating Canada’s Mortgage market is becoming more challenging, but not impossible. However, I think this rule change is prudent, considering our diverse National Real Estate market is. I also think your friends, family and co-workers might like to learn about our coming rule changes. If so, share this blog post with them. Also, please share this on Facebook.

Thank you,

Chad Moore

Here are some Calgary Real Estate numbers, across all property types, out of the gate for…

Hey Guys! Tariffs are here. Now what? Tiff Macklem, governor of the Bank of Canada, gave…

Hey Guys! The Bank of Canada publishes "meeting deliberation notes" relating to the discussion of raising,…

When the governor of the Bank of Canada speaks, we listen! Tiff Macklem, governor at…

Let's look back at January 2025 Calgary Real Estate Board (CREB) data to make sense…

Hey Guys! Here's an example of how the Bank of Canada is in a balance…

{kind=link}