If you open this email, scroll down and see all the text and charts …don’t auto-delete this. Stick with me here.

You know I like to keep things simple for you (and balanced).

Trust me here, read this (oh, and wu-tang is forever) …

Credibility in the central banking world is vitally important. Financial markets, asset values and sometimes families make decisions based on forward guidance from our central bankers. Over the past couple of years, trust has been broken.

Why?

We all remember the “unusually clear” forward guidance from governor of the Bank of Canada, Tiff Macklem, back in July 2020. The forecast was “low rates until 2023“. Then when we were experiencing rising inflation, that was labeled as “transitory“. Remember all this?

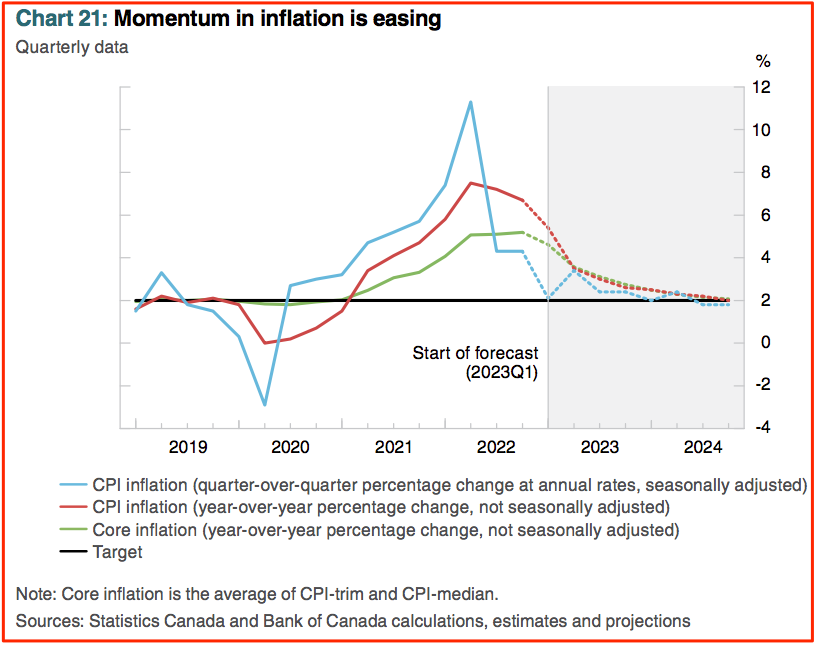

The Bank of Canada’s January ’23 Monetary Policy Report (MPR) was forecasting inflation to be at around 3% by summer. With the backdrop of broken trust, and lost credibility, I was skeptical.

Perhaps my skepticism is relaxing with Canada’s most recent inflation data? Let’s take a look …

The most recent consumer price index (CPI) report is generally inline with Bank of Canada expectations.

The BoC has three core measures of inflation that are all coming down:

1. CPI-trim: 4.8%

2. CPI-median: 4.9%

3. CPI-common: 6.4%

4. Total CPI: 5.2%

Note, the key policy interest rate is 4.50%. The commercial bank prime rate is 6.70% (this rate is what variable rate Mortgages, and HELOC’s are based from).

Well, that depends (sorry). I’ll frame this keeping in mind a) I’m speaking in generalities, and b) I’ll remain balanced (duration of higher rates and a reduction of rates). Cool?

The Bank of Canada’s mandate is low and stable inflation (1-3%), with the backdrop of a fully functioning economy (jobs market, GDP etc).

The down trend of inflation is positive for future rate cuts because it lessens the requirement for this high (restrictive) interest rate.

Let’s be reminded …we know the Bank of Canada can’t move too far from the U.S. Federal Reserve. They just raised rates 0.25% with forward guidance indicating more rate hikes are reasonable to expect (data dependent).

Barring any sudden or unanticipated economic shock—I’m finding the general market consensus is we are nearing peak interest rates.

Here’s a new chart for you …the U.S. 2-year treasury yield curve has an uncanny relationship with the U.S. Federal Reserve central interest rate.

Looking back, each time the 2-year treasury yield has risen (blue line), or lowered, the U.S. Fed rate (orange line) follows suite. These two curves just crossed (the 2-year yield crossed below the Federal Reserve interest rate) which is a leading indicator of the U.S. Federal Reserve cutting rates (sometime soon).

I am fully aware that I can showcase any data I want to support a choosen narrative. So, here is a case for rates to remain at today’s levels …

Past Learnings Remembered …

I wrote you a couple months ago about the double dip inflationary run in the early 1980’s. During that inflationary period, rates rose and inflation responded by coming back down (seems similar to today). At that time, the central bankers lowered rates too soon (with the benefit of hindsight), and then inflation came ripping back …then the interest rate environment really got ugly (hello 20% rates, oops).

It is possible the duration of high rates remain with us until inflations “back is broken“. Honestly, I would prefer duration at these interest rate levels than, the euphoria of lowering rates too soon, and the gloom of another rate hike cycle—that would likely be even higher.

What about fixed rates …

Recently, fixed Mortgage rates peaked early in January, then ground lower until about late-January, then started ascending again, until recently. It’s been a yo-yo ride (image below).

With the U.S. banking crisis about 10 days ago, investors have been fleeing to the safety of bonds. This raises the price of bonds, lowers bond yields (prices and yields are the inverse) which all lowers Mortgage rates.

But (there is always a but .. ;-)) Mortgage rates have not exactly fallen with bond yields.

Why?

I have a couple ideas …1) financial instability, 2) profit, 3) higher capital cost requirements.

The Office of the Superintendent of Financial Institutions (OSFI) is surveying industry members about possible changes to better serve the entire financial system.

I think one of these changes is having commercial banks keep more capital reserves, as a percentage of loans, on their books. More capital on hand secures the financial system. What is one way to keep more capital? Increase the profit margins of Mortgage lending of course (I.E., higher fixed rates).

Ok, let me grunt out a two sentence update on this whole email …1) Variable rates might go up or down, and 2) Fixed rates are a rollercoaster.

Honestly though, there is a lot going on than can swing the market either way. Here’s what’s important …

I hope this is helpful! Share this info, if you think someone else might enjoy it. Reach out if you have any Mortgage needs (sale, purchase, refinance, renewal, rental, second home etc).

Cheers,

Chad Moore

P.S.

Are you planning to sell your home, and transition? I have an in-depth video for you!

Are you a buyer? This group of videos and reports will be good for you!

P.P.S.

I write content for you as a way to add value, and become a trusted source of information. Then when you think of Mortgages, you think of me.

Or, I could buy a big billboard on the side of the highway like this Realtor in Colorado. Wu-Tang Is Forever! ;-)

Here are some Calgary Real Estate numbers, across all property types, out of the gate for…

Hey Guys! Tariffs are here. Now what? Tiff Macklem, governor of the Bank of Canada, gave…

Hey Guys! The Bank of Canada publishes "meeting deliberation notes" relating to the discussion of raising,…

When the governor of the Bank of Canada speaks, we listen! Tiff Macklem, governor at…

Let's look back at January 2025 Calgary Real Estate Board (CREB) data to make sense…

Hey Guys! Here's an example of how the Bank of Canada is in a balance…

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}