Here is a summary of Canada’s latest “Monetary Policy Report“, released from the Bank of Canada (BoC). Alberta’s economic summary data is also below.

Consider forwarding this email to others who might appreciate this simple summary.

[If you’re new and would like access to my distribution email list, email your request to me. Thank you.]

National Economic Summary:

- GDP forecast has increased from 2.0% to 2.1% for 2017.

- Growth is underpinned by rising employment in the service sector, household incomes and consumption.

- Jobs concentrated in part-time employment remain firm. However, total hours worked and wage growth are not growing at the same pace as the U.S.

- Export growth is expected to increase. Canada’s currency is depreciating relative to the Greenback. However, the Loonie is still relatively strong compared with other Global currencies. Because of this the Bank of Canada might consider an interest rate cut, lowering the value of our currency.

- Total consumer price index (CPI) inflation is expected to be near 2% through 2017 & 2018. This offsets the effects of higher consumer energy prices and lower food prices.

- Interprovincial migration TO Alberta was a net inflow of 10,000 people in Q2 2014. Compare that with 4,000 net outflow in Q3 2016.

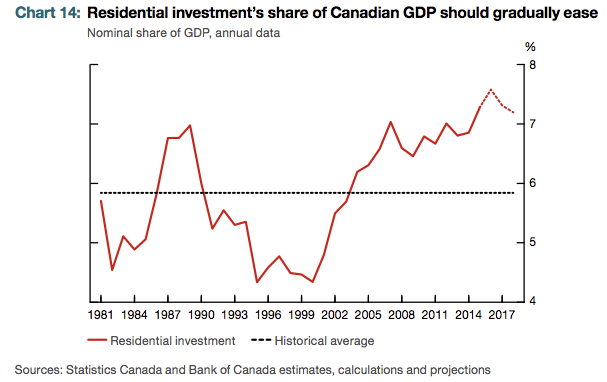

- Residential investments share of Canadian GDP is expected to gradually ease. This is partially due to constricting Mortgage rule changes and Provincial Real Estate regulation. See chart 14.

- Household spending is down in energy-intense Provinces and holding relatively on a National level. See chart 13.

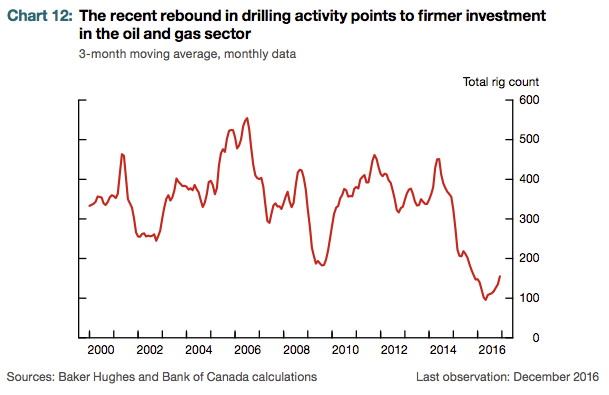

- It seems that oil drilling activity has bottomed out and is rising again. See chart 12.

National Charts Of Interest

International Economic Summary

- Stronger U.S growth prospects are raising indicators of business optimism and consumer confidence. This is due to an anticipated shift in fiscal policy, albiet the nature and timing of anticipated changes are uncertain.

- U.S energy investment is anticipated to support the recovery of capital expenditures. Higher oil prices lead to increased drilling activity.

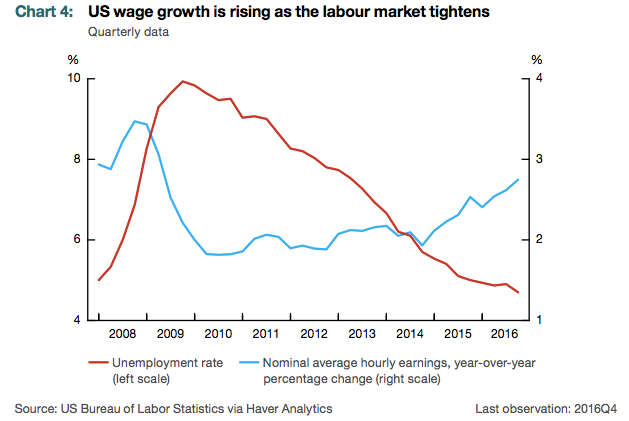

- U.S consumption is expected to remain healthy based on strong labour market and gradual increase in wages. See chart 4.

- The Euro area economy is holding, despite financial system stresses and elevated political uncertainty in some areas, particularly around Brexit. Future growth is also limited by labour market rigidities.

- The Chinese economy is on a sustainable growth path. Business investment is expected to slow with reforms to state-owned enterprises continuing. Steps to control overcapacity mining and manufacturing sectors are taking place.

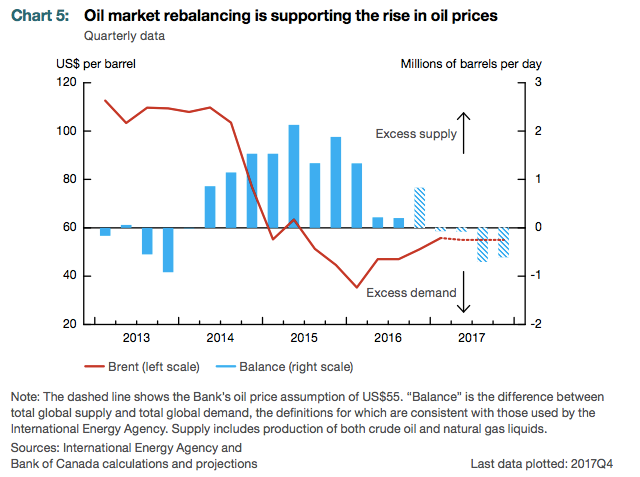

- OPEC has cut oil production to hasten rebalancing of the oil market. Risk to the oil market is lower because prices are below levels required to support medium market rebalancing. Anticipating sustained higher pricing is limited because technology improvements have reduced costs for unconventional oil (U.S shale). See chart 5.

Alberta Labour Market Summary:

- December 2016 saw a gain of 6,900 jobs following a loss of 13,000 in November. Full time employment gains outpaced the loss of part time positions. The majority of job gains have been from self-employment and public sector.

- Alberta’s unemployment rate fell 0.5% to 8.5% reversing the gain from the previous month. The National unemployment rate rose 0.1% and is 6.9%.

- In Alberta, data from October 2016 saw average weekly earnings (AWE) decline 0.9% to $1,106/month from the previous month. Alberta AWE were down 2.6% year-over-year. National AWE is also down 0.1% to $954/month. National AWE is unchanged year-over-year.

- I think on the leading edge of economic downturns, Edmonton’s unemployment rate is higher than Calgary’s. I think in leading edge economic up-cycles, Edmonton’s unemployment rate is lower than Calgary’s. I think the correlation between employment and drilling activity, linked with Edmonton’s labour market is more sensitive than Calgary’s. Time will tell.

Mortgage Rules & Credit Update:

- With very recent Canadian Mortgage rule changes, detailed in my coming Calgary Real Estate & Mortgage Newsletter, fixed interest rates are rising. This is due to the Mortgage lender’s cost of funding a Mortgage and the Canadian Bond market.

- Interest rate pricing discrepancies between insured, insurable and conventional Mortgage files are very different. This relates to the loan-to-value of your Mortgage file.

- Mortgage insurance premiums are also rising. This is reactionary to Government Mortgage rule changes requiring more capital to be in reserve, available to backstop a housing melt-down. Banks are also now required to retain more capital on hand for such an event.

- One looming Mortgage rule change I am anticipating is Mortgage insurance premiums being based on down payment percentage AND the applicants credit score. Know this, the repayment history and utilization (maintaining low balances on credit instruments) equal ~65% of the overall credit score. Please take care of your credit rating.

Conclusion:

I think the majority of data released from the Federal and Provincial governments is not overly positive, exciting or optimistic. On the flip side, I am not understanding this data to be sharply negative either. For me, I’m starting to think there is light at the end of the tunnel :-).

Thank you for reading, referring and trusting me with your Mortgage business.

Talk soon,

Chad Moore