Hey Guys!

The Bank of Canada is set to make a rate announcement on 25 January 2023—their first of 8 rate announcements this calendar year.

There is anticipation of another 0.25% rate hike—heads up!

Let’s go around-the-horn, economically, for a lay of the land …

1. Inflation.

2. Bond market.

3. Previous BoC commentary.

Let’s GOOO!

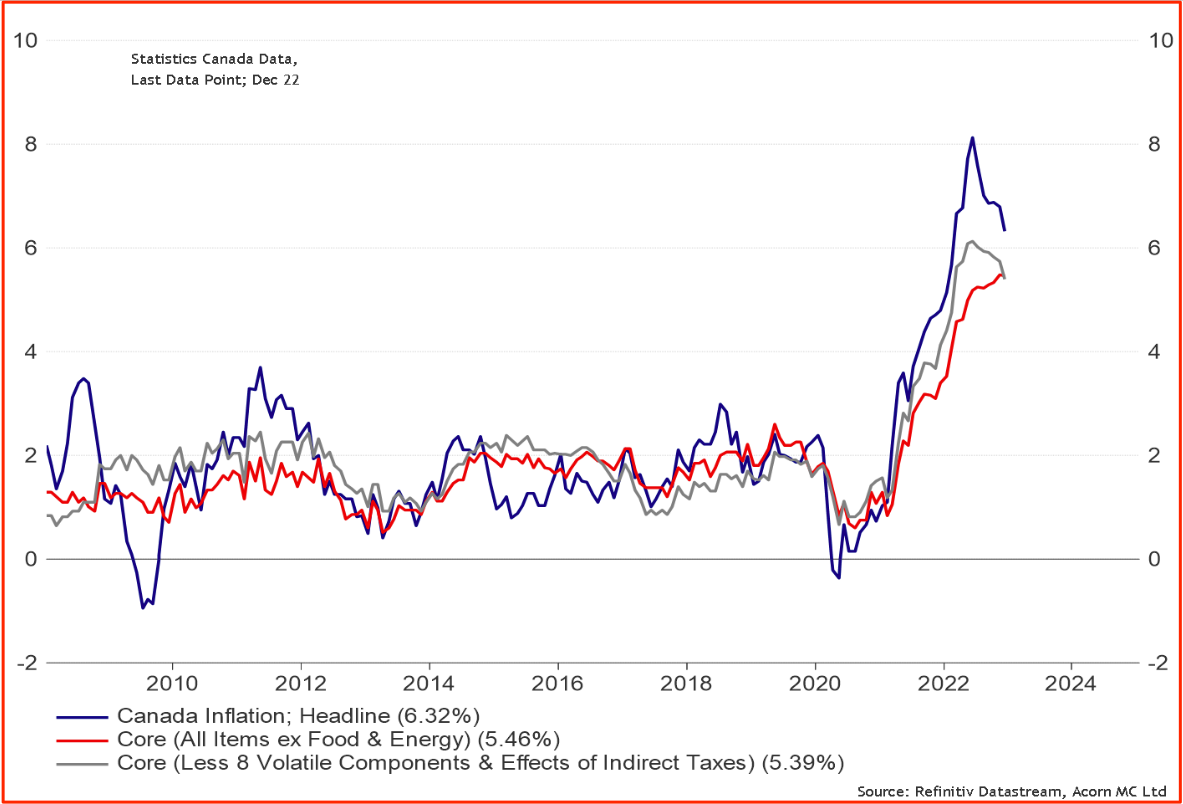

Inflation Past Peak—But Irritatingly High

Inflation continues to move off it’s 40 year peak, but remains irritatingly high for our policy makers. The mandated inflation target is 2% so we still have a long way to go (chart #1 below).

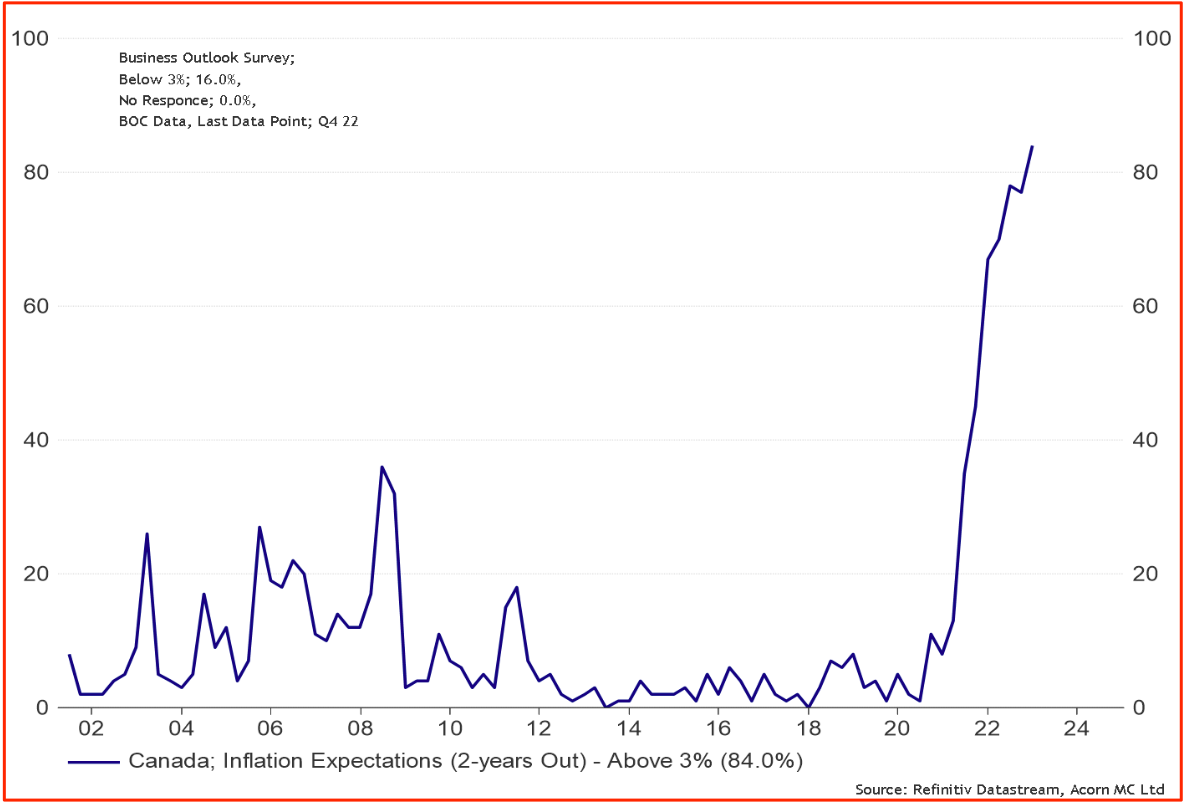

Inflation expectations are also sky high (chart #2 below)! This is an indicator of sentiment across Canada. The issue the Bank of Canada has with inflation expectations is it effects consumer behavior …if people think prices will be higher in the future, there is a tendency to pull purchase demand forward. Doing this, is inherently inflationary therefore making higher prices a self fulfilling prophecy.

This is what “un-anchored inflation expectations” look like and I bet this is very bothersome to our central bankers.

Core measures of inflation are also rolling over, off their recent peaks. However, the rate of change seems to be rather sticky.

Bond Market—Headed Lower (for now)

The Canada 5-year bond yield is rolling over, steadily grinding lower. Remember, fixed interest rates are set largely off movements in the bond market.

We are in an era that is rather counter-intuitive …the Bank of Canada is raising interest rates, yet fixed interest rates are falling. Many people reading news headlines might miss this distinction.

Below is a bond yield chart looking back 1-year. We can see the rapid rise of bond yields last Spring. Then a dip last Summer. We are approaching that Summer low, which might prove to be a resistance point.

There is another chart below showing a 5-year look back of Canada bond yields. I mention this because I’m currently reminded of 2019. We saw a rather strong rise in bond yields in 2018, then a steady drop of yields throughout the first 6 months of 2019. There is no need to re-cap the fall of bond yields in 2020 ;-).

There is a possibility bond yields grind lower as more evidence of recessionary pressures mount. Let’s watch. If this plays out, I see an possible opportunity for variable clients to consider locking into a lower fixed rate. Please note “possibility” and “possible opportunity”. Please contact me for specifics.

Bank of Canada—Commentary

1. Rate hikes are NOT on auto-pilot anymore.

The press release from the Bank of Canada December 2022 stated, “it will be considering whether the policy rate needs to rise further“.

Deputy governor Kozicki furthered this sentiment by saying, “we are moving from how much to raise interest rates, to wether to raise interest rates“.

Another way to summarize this is, the BoC is being more data dependent. The market consensus I’m seeing/hearing about is another 0.25% rate hike this week.

2. The Bank of Canada can’t/won’t stray too far from U.S. Fed.

Deputy governor Kozicki stated in December 2022, about 50% of inflation is from foreign forces outside of our control—I.E., the United States!

The U.S. consumer carry’s less debt than Canadians and the overall economy is less reliant on interest rate sensitive areas of the economy—housing. This might create a scenario where U.S. interest rates remain higher for longer to rein inflation in.

The U.S. Federal Reserve is making a rate announcement January 31st.

3. Quantitative tightening is ongoing.

Scroll up and take a look at the bond yields from back in 2020-2021. Why so low? Quantitative Easing (QE). Bond yields were artificially low to stimulate the economy. Now we are in an era of quantitative tightening (QT).

The tightening happens when the Bank of Canada allows bonds to roll off their balance sheet at maturity. These bonds are available for purchase in the secondary market.

With Canada’s central bank not purchasing these bonds, the demand for them is less. We know this from simple economics …less demand is downward pressure on prices.

Stay with me here …

Bond prices are the inverse of bond yields. So if there is less demand, and an increase of supply, prices drop—yields rise—and fixed Mortgage rates rise.

But Chad, didn’t you state above that fixed rates could come down? Yes. The tendency is, during fear of recession, investors search for the safe haven of bonds as a form of security. So there is an increase of demand to purchase bonds… higher demand, raises prices, drops bond yields, and drops Mortgage rates.

There are many macro-economic forces at play here. Please read general tendencies and function—not necessarily prediction.

Conclusion:

I can’t help but think of a favorite quote of mine. This is from Jim Rohn, an original gangster (OG) in the personal development space—from the 1980’s. I think he’s got great content from his seminars back then, which can be found on YouTube.

Jim stated he always could predict the future …it’s “opportunity mixed with difficulty“. And that’s what I see for Calgary’s Real Estate market—opportunity mixed with difficulty.

Plan for a rate hike of 0.25% this week from the Bank of Canada. Do not confuse that with slightly lower fixed rate Mortgages. Help your friends and family understand the difference :-).

If you’re planning to purchase, or sell and purchase. Reach out so we can start planning together.

Cheers,

Chad Moore

P.S.

Keep those NY resolutions going strong!!