Hey Guys!

Let’s look at some leading economic indicators to help us understand where inflation might trend, and relate everything back to Canadian Mortgage interest rates.

Read below:

This information is a part of the short term debt/credit cycle. In case we needed a reminder, this cycle (loosening or tightening of monetary policy) is a primary driver of the Real Estate market.

I think in many people’s mind the Bank of Canada lost credibility as we are exiting the pandemic because of:

It seems the Bank is now regaining their credibility by forcefully raising interest rates to brow-beat inflation back to the 2% target. Collateral damage in the economy (I.E., housing) is an afterthought—the mandate of 2% inflation is the goal.

I think the Bank will achieve their inflation target sooner than they plan, which is by 2024. Just as quickly as money can be created out of thin air (I.E., creation of money through credit); money can also be destroyed with debt pay down. With the cost of borrowing going up—this is exactly what is happening!

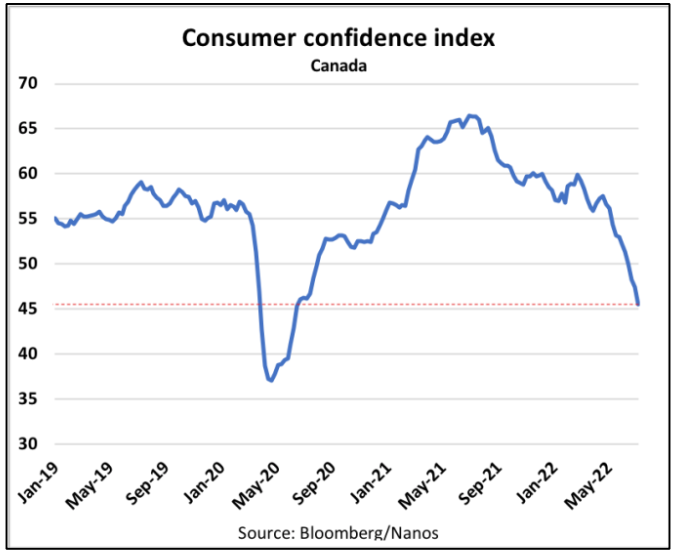

Here are some indicators of possible peak inflation, and more:

One fascinating fact about inflation is how influencial inflation exceptions are—which relate to consumer spending. If I think prices will be higher in the future, I pull forward my spending (consumer/business). This, in and of itself, is inflationary because more money is spent driving prices higher. I’m keeping an eye on business and consumer inflation expectations. So far, they remain above the BoC’s 2% target.

And this brings us back to the Bank of Canada’s credibility …if people really think the BoC will hike rates into a potentially slowing economy just to bring inflation to heel—spending decisions are likely to be altered (I.E., lower). This will bring inflation down, regaining credibility. Question: are you changing your spending habits because of higher rates (yet)?? I am.

Of all the news articles relating to inflation/BoC monetary policy etc, I found this one very clear and simple. I like that ;-).

Let’s start with two fundamentals, which are understanding:

1. Adjustable rate Mortgages (ARM).

2. Variable rate Mortgages (VRM).

Adjustable rate Mortgages (ARM) adjust when the Prime interest rate moves up or down. The clients Mortgage payment changes which retains their repayment timeline (amortization).

Variable rate Mortgages (VRM) have a static payment. The payment does not change with the movement of the Prime rate. When the Prime rate increases, less of the clients payment goes to principal pay down with more going to interest.

This can be a problem though. Here’s why …

The trigger rate!

What’s this? A trigger rate will only apply to VRM in an increasing interest rate environment. Here’s how a trigger rate would come into effect …if the Prime rate increases to a point where the clients static Mortgage payment does not cover the interest cost of the payment. In this scenario, the Mortgage would GROW, and not be paid down. The lender will then call to fix this scenario requesting either a) a lump sum Mortgage payment to lower the balance of the Mortgage, or b) a payment increase to cover more of the required interest payment.

VRM lenders are:

Heads up—with another Bank of Canada rate hike planned for September, trigger rates could be enforced. Ask people in your network if they have a VRM or ARM. Then ask them if they are prepared for a trigger rate. If you have a VRM, I recommend increasing your Mortgage payment before being forced to.

Realtors reading this email—tell your past clients about this possibility and to connect with their lender. Surprises in Real Estate are not good, even as a homeowner.

The super sized interest rate hike by the Bank of Canada was met with a blank stare from the bond market.

You see, the Bank of Canada is chasing a lagging economic indicator, inflation. And they need to at this point. However, the Bond market is forward looking and bond yields are not moving.

I’m seeing some lenders cut fixed interest rates in response to bond yields falling.

I am thinking of this inflationary period like a bell curve (not necessarily symmetrical though). You know the one—low on the edges, rising in the centre. I think it is possible our current inflationary data is near the middle chunk of the bell curve right now. I’m keeping an eye on leading inflationary indicators for you.

With higher rates, variable rate Mortgage holders could face a trigger rate scenario. I’m reading this would likely be a shock to many—in terms of knowledge AND finances—but not a massive cash-call or payment hike.

Fixed rates seem to have plateaued, and are even grinding lower at some lenders for the moment. This provides some relief for Mortgage renewals, and new buyers.

I hope this is a helpful update for you! Reply to this email with any questions or concerns etc. Your emails come directly to me.

Talk soon,

Chad Moore

P.S.

This is a bumper year for mosquitoes hey! My canoe trip was great, but man did I have to deal with a lot of bugs. I’d prefer bugs versus a dry/fire summer with smoke in the air!

P.P.S.

I was successfully drawn for a special hunting license for this Fall! I’m pumped about that!

P.P.P.S.

August long plans—what are you up to??

P.P.P.P.S.

B.C. Real Estate just implemented a mandatory “3 day cooling off period”. This means buyers can back out of a Real Estate purchase within the first three days. At this time, I do not see anything like this looming for Calgary’s Real Estate market. Link to the press release below:

https://news.gov.bc.ca/releases/2022FIN0026-001134

*If you find this newsletter helpful, pass it along. Thank you for your new business, repeat business and referrals*

Here are some Calgary Real Estate numbers, across all property types, out of the gate for…

Hey Guys! Tariffs are here. Now what? Tiff Macklem, governor of the Bank of Canada, gave…

Hey Guys! The Bank of Canada publishes "meeting deliberation notes" relating to the discussion of raising,…

When the governor of the Bank of Canada speaks, we listen! Tiff Macklem, governor at…

Let's look back at January 2025 Calgary Real Estate Board (CREB) data to make sense…

Hey Guys! Here's an example of how the Bank of Canada is in a balance…

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}