Hey Guys!

This is a monetary policy update from the U.S. which influences the Bank of Canada (BoC) and ultimately Canadian monetary policy (interest rates).

I know we are all facing higher interest rates that are effecting folks in various ways …a) adjustable Mortgage payments are higher, b) variable Mortgage payments are weighted more to interest, c) people renewing their Mortgages are facing higher rates and d) new home buyers are qualifying at much higher rates!

Higher rates are seeping into households from other angles too …a) personal lines of credit rates, b) student loan rates, c) auto loan rates, d) business and commercial loans.

We are all feeling the squeeze, so you’re not alone.

Let’s start with the basics and review what the U.S. is up to and what could happen in Canada …

The Federal Open Market Committee (FOMC) is a branch of the Federal Reserve System. The Federal Reserve (Fed) controls monetary policy in the U.S.

Last week Jerome Powell, chairman of the Federal Reserve (Fed), announced the U.S. is raising interest rates. This is a summary of his comments.

- U.S. Fed raises the neutral interest rate to 2.50%. A neutral interest rate is believed to be neither stimulative OR restrictive. The current Fed rate is now 3.00%-3.25%. This means the U.S. Fed rate is now “restrictive”.

- Jerome Powell provided forward guidance there are further U.S. Fed rate hikes coming. The Fed’s inflation target is also 2% with them firmly focused on that target.

- The FOMC’s 19 members, on average, anticipate the Fed to raise rates by another 1.25%.

These estimates have been incorrect before. As recently as 1-year ago the 19 members anticipated interest rates would only rise by about 1.00% (that was blown out of the water!).

Yes, there is stern language, and a reasonable probability of another 1.25% rate hike by U.S. policy makers, but that does not mean 100% certainty. - In addition to continued rate hikes, the Fed plans to significantly reduce its’ balance sheet.

Central bank balance sheets exploded from pandemic related spending. In the U.S., this was accomplished with the Fed purchasing treasury notes (similar to the BoC purchasing government of Canada bonds).

The Fed plans to unwind their balance sheet which indicates a tendency of a further rise of fixed Mortgage rates (more on that below).

This is important because U.S. monetary policy greatly influences Canadian monetary policy. The old adage is, “when the U.S sneezes, Canada catches a cold“.

Here’s how the U.S. extended rate hike cycle can impact the Bank of Canada—and ultimately Canadian Mortgage interest rates:1. Canada follows in lock-step as the U.S. Fed hikes rates. I’m hearing from other market participants that Canada’s monetary policy is closer to the top of the rate hike cycle than the U.S.

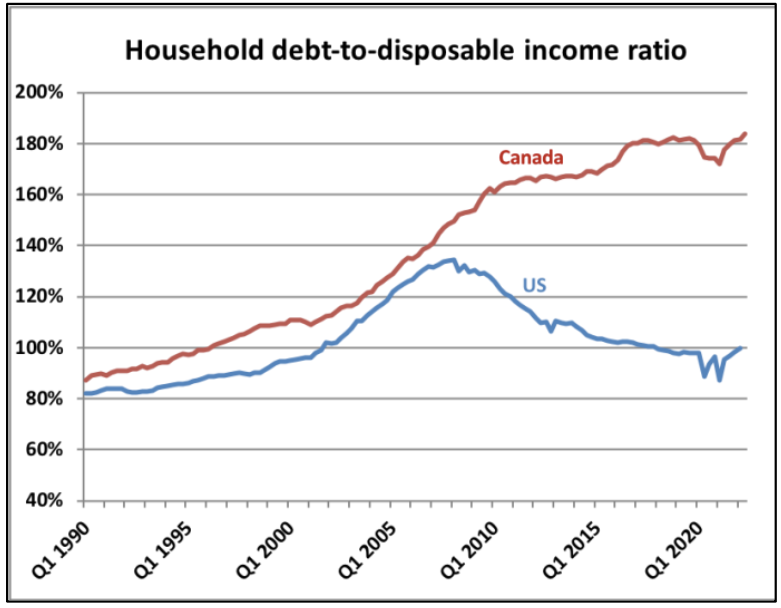

Canada’s debt to GDP ratio, reliance on Real Estate and related income are the first to change in a rate hike cycle. Canada’s economy is significantly more coupled with these industries therefore making the effects of following the Fed higher more painful in Canada.

2. The Bank of Canada does not hike rates to match the U.S Fed. If the BoC does not hike interest rates that closely match the Fed, Canada’s currency has the tendency to fall.

This creates pitfalls and opportunities for Canada’s economy. A) Our primary trading partner is the U.S. so imports become more expensive which is inflationary. B) Our primary export partner is also the U.S. so our exports become more attractive to purchase.

Formally, central bankers DO NOT actively participate is currency manipulation. Currency movements are collateral damage from various macro-economic happenings.

3. Canada imports higher fixed Mortgage rates. Remember, fixed interest rates move based on bond yields. Bond yields move based on bond prices. Bond prices are greatly influenced by central bank monetary policy.

A simple example of this is the recent pandemic. We saw this when central bankers purchased bonds which raised bond prices, lowered bond yields and lowered fixed Mortgage interest rates. Remember those pandemic era fixed Mortgage rates of 1.99% (or lower)—that was an artificially lowered interest designed to stimulate the economy (I.E., housing market, and it worked!).

Well, central bankers (Fed & BoC) are purchasing less bonds—even allowing bonds to be removed from their balance sheet. The tendency is other bond purchasers are left to pick up the slack and purchase more bonds. Without central governments purchasing these bonds, demand is not there. In this scenario (less demand) the tendency is, bond prices fall, bond yields rise and therefore fixed Mortgage rates rise. The tendency is as U.S. treasury yields rise, government of Canada bond yields rise in sympathy. This is something to watch!

Canadian Mortgage qualifying is based on the “stress test” interest rate. The stress test rules are as follows …home affordability (Mortgage qualifying) is based on the clients ability to pay their Mortgage AS IF their interest rate is the contract interest rate + 2.00%.

If fixed rates continue to grind higher, the stress test rates simultaneously rise. I’m sure you can imagine how qualifying AS IF your interest rate is nearly 7% is a headwind to home affordability (assuming everything else being equal).

Conclusion:

We continue to exit the pandemic with as much, if not more, economic uncertainty as we faced entering the pandemic. Do you remember the uncertainty of April 2020?

I think it is possible we look back on this era of monetary policy and witness central banks over tightening interest rates. How high and for how long these rates remain elevated is anyones guess.

The U.S. Fed and BoC are hellbent on bringing inflation down to the 2% target. I think they’ll get there. At what economic cost will be written in history.

Let’s all thank our lucky stars we live in Calgary! Our province is still experiencing net positive inter-provincial migration which supports housing demand (purchase & rental), strong oil and gas sector (job support and trickle down economics) and a growing tech community (employment diversity).

I hope this is helpful? If so, consider sharing this with folks who might appreciate it.

I’ve had several referrals come through from you readers—thank you!

If you have any Mortgage or Real Estate related questions, let me know!

Cheers,

Chad Moore

P.S.

I’m starting a short-term diet heading into Thanksgiving so I feel good about eating unapologetically ;-).